Supporting Coffee Value Chains and Climate Finance

An Introduction to Coffee

Coffee production is a highly vulnerable sector, with many pressing challenges, both directly and indirectly, related to climate change. Climate change itself is expected to reduce worldwide yield and decrease coffee-suitable land by 50 per cent by 2050.

Charlie Martindale, Analyst at Globalfields Ltd

Coffee has a long history. Legend has it that the drink originated in 9th century Ethiopia, when a goat herder noticed that his animals could not sleep after consuming the berries of a particular tree. Several hundred years later, in the 15th and 16th centuries, coffee culture began to spread rapidly across what is now known as the Middle East, with public coffee houses readily accessible to citizens of Yemen, Iran, Egypt, Syria, and Turkey, forming social hubs where people gathered to chat, listen to music, watch performances, and keep up with news and politics. Throughout the following centuries, the proliferation of the crop and its associated culture spread to every major region on Earth, becoming the second most profitable export crop in the world in the 19th century, behind only crude oil.[1]

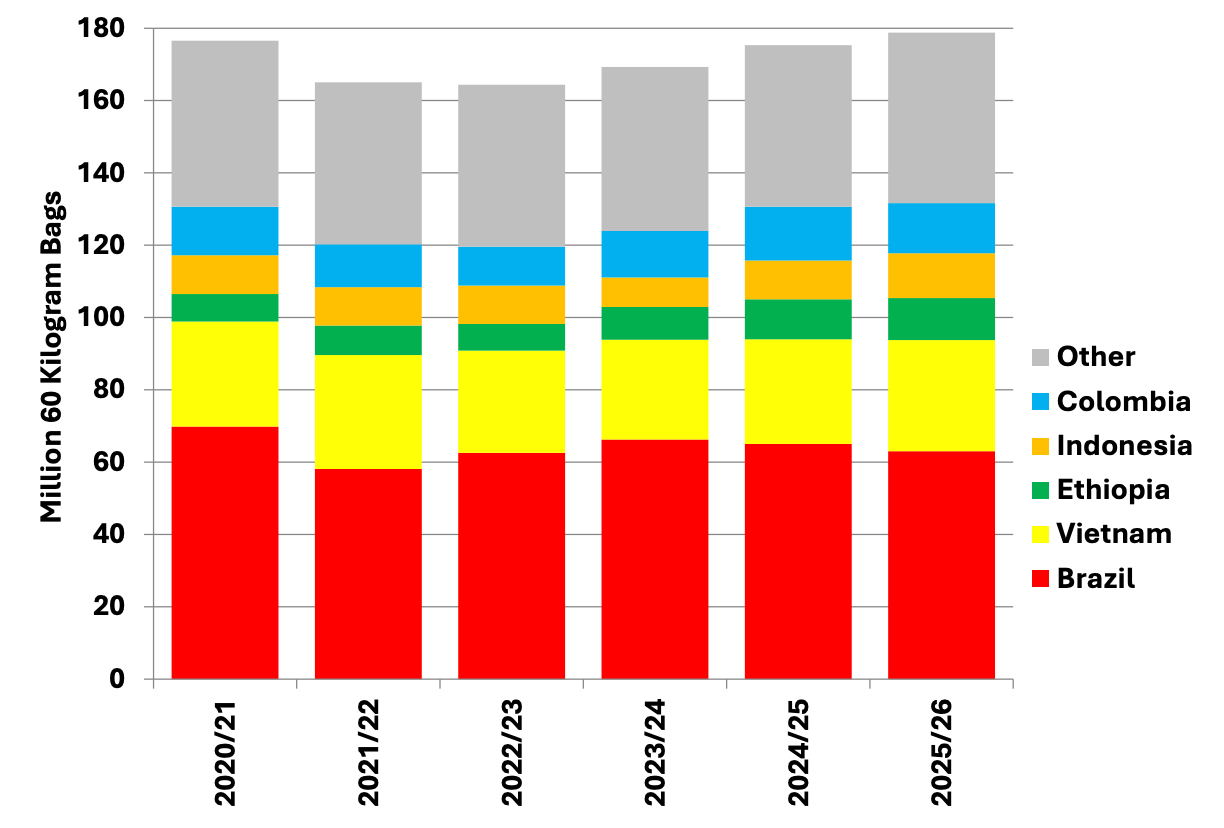

Fast forward to the present day, coffee consumption stands at a staggering 173.9 million (60kg) bags a year, with FY 2025/26 forecasted to be a world record production year at 178.8 million bags, as shown below in Figure 1.[2] To put this into a national perspective, the UK drinks 98 million cups a day, with 80 per cent of households purchasing instant coffee, and the same percentage visiting coffee shops at least once a week.[3]

So, what is the link between such a ubiquitous commodity and climate finance?

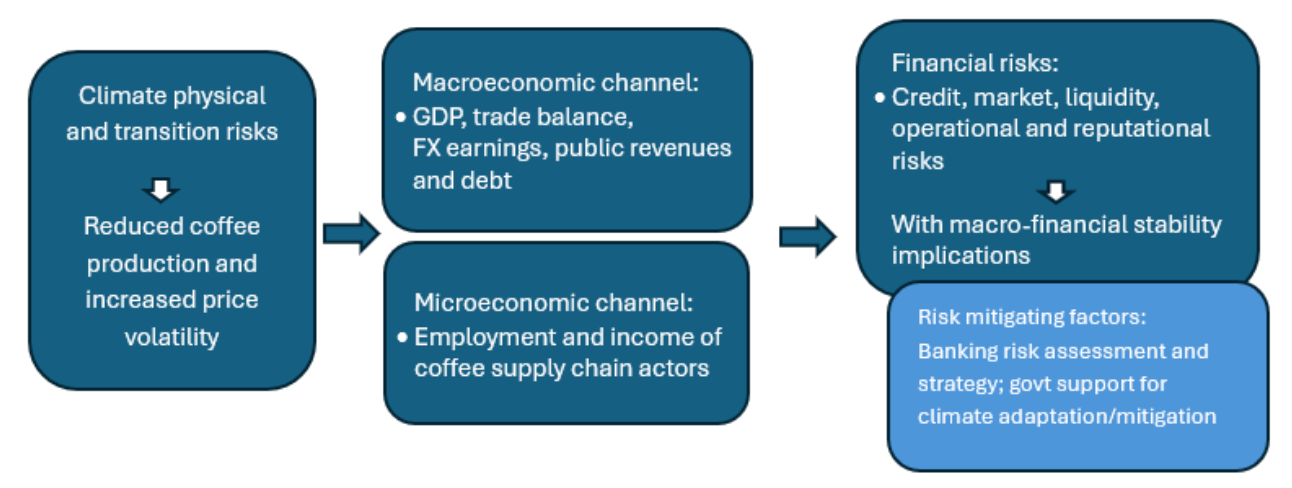

The answer may be more pressing than many coffee drinkers realise. Coffee production is a highly vulnerable sector, with many pressing challenges, both directly and indirectly, related to climate change. Climate change itself is expected to reduce worldwide yield and decrease coffee-suitable land by 50 per cent by 2050, according to projections by the Intergovernmental Panel on Climate Change (IPCC), with wide-ranging consequences across “water, crop, and nutrient management: drought, salinity, biodiversity decline, suitability losses, change of species seed availability, resistance to abiotic and biotic stressors, etc”.[4] Farmers are already feeling the heat, as the top five coffee-growing countries, responsible for 75 per cent of total production, are experiencing 57 additional days of coffee-harming heat annually because of the climate crisis[5], reducing yields, raising prices, and harming the employment and income of coffee supply chain actors.

Research into the impacts of climate change on coffee bean growth also reveals that increases in mean maximum temperature and mean precipitation, alongside variation in precipitation patterns, have a significant impact on the probability of below average bean size and above average bean defects. Here, under the Shared Socioeconomic Pathway SSP5-8.5 (often referred to as the ‘business as usual’ warming scenario), an increase in the mean maximum temperature of 1.3°C by 2050 compared to 2010 levels during the flowering season would lead to an increase of the likelihood of small bean size by more than 30 per cent, having a negative impact on the coffee quality and taste, thus on the coffee price and farmers’ livelihoods.

Additionally, an increase in mean precipitation during the harvest season by 15 per cent by 2050 leads to an increase in the likelihood of bean defects by around 10 per cent, while the decrease in the mean precipitation during the early growing season by 5 per cent by 2050 leads to a decrease in the likelihood of small bean size by around 9 per cent.[6] That is to say, overall, the impacts of climate change clearly have a significant negative effect on the production, size, and quality of coffee beans compared to today, and therefore on the earning potential of smallholder farmers and other independent actors in the coffee value chain.

Further, the vulnerability of coffee-growing areas is exacerbated by many other factors, including land size, income levels, labour availability, postharvest infrastructure, access to markets, technical and financial assistance, and so on. Together, the combined threat of climate change and these factors necessitates that coffee producers implement integrated management practices on their farms to ensure the long-term viability and sustainability of production.

Potential approaches could include significant investment in plant renovation, improvements to agricultural processes through the introduction of circular and regenerative practices, and more effective marketing systems[7]. But how should smallholders approach this challenge, particularly given the aforementioned constraints, including significant technical and financial limitations? And what are the appropriate vehicles of climate finance in the sector, which aims to support and fund mitigation and adaptation activities, particularly in areas most vulnerable to climate change?

Climate Finance Initiatives supporting coffee value chains

Smallholder farmers, who produce 60-80 per cent of coffee worldwide, received just 0.36 per cent of the funds needed to adapt to the impacts of climate change in 2021.[8] Current initiatives in the climate finance space therefore seek to address the gap in financing climate-resilient coffee production between these smallholders and large commercial estates and plantations. The underlying ideology of this approach is that by enhancing access to financial instruments and ensuring stable contractual relationships, particularly for the provision of timely pre-harvest working capital, we can unlock pathways to scale adaptation and mitigation through the implementation of climate-smart production and sourcing. The added benefit of implementing climate-smart approaches is that they enhance producers' ability to manage and adapt to price volatility, providing greater macroeconomic stability to the GDPs and trade balances of significant coffee-growing countries worldwide.[9] [10]

Key initiatives to finance the coffee sector have therefore emerged in blended finance contexts, combining public and private sector resources to deploy ‘substantial and transformational’ funding, primarily for smallholders and independent roasters. Yet, these have been fairly limited in scope and size, oftentimes components of larger smallholder-focused de-risking funds with limited focus on coffee, such as the IDH Farmfit Fund (committing USD 10 million to unlock trade finance for coffee and cocoa producer organisations in Latin America and the Caribbean), or limited in geographic reach, such as the Root Capital Coffee Resilience Fund (limited to USD 7 million to enhance farmer resilience in Central and South America).[12]

However, some progress in this department has been made, with the GCF accepting the USD 212 million Food Securities Fund Accountable Cocoa and Coffee Tranche (FSF ACCT) at the last Board meeting (B.44) in March 2026. This project specifically focuses on coffee and cocoa value chains, targeting one of the most binding constraints in these sectors: the structural lack of timely pre-harvest working capital for midstream actors (cooperatives, processors, traders, and exporters) that aggregate (i.e. collect, consolidate, and organise agricultural produce, while leveraging existing business relationships with Value Chain Partners) from smallholders. By scaling access to sustainability-linked, short-term renewable financing, alongside targeted Technical Assistance (TA), the FSF ACCT aims to unlock climate-smart production practices at the farm level while strengthening supply chain resilience.

In the context of coffee, this represents a meaningful step towards scaling finance for smallholder-linked systems. By tying access to working capital to compliance with environmental and social criteria, including zero-deforestation commitments and climate-smart agriculture, the FSF ACCT creates a direct financial incentive to improve land-use practices, reduce emissions, and enhance resilience. Further, the TA component, at USD 6 million, provides significantly greater direct support to smallholders than existing projects, ensuring efficient adoption of climate-smart interventions in agroforestry, soil health, traceability, and climate risk management.

Moving Forward: Closing the Financing Gap

The FSF ACCT model signals a shift towards more integrated, value-chain-based financing models that are scalable and aligned with climate objectives. If successfully implemented, it could provide a replicable blueprint for mobilising institutional capital for coffee and other climate-sensitive commodities, addressing both the financing gap and the underlying structural barriers to sustainable production.

Globalfields has been engaged in supporting a number of institutions in addressing blended finance needs and structuring the most relevant concessional instruments to support small farmers and the coffee value chain. Moving forward, the sector’s sustainability will likely depend on expanding into a more diversified financing ecosystem, including greater direct access to finance for smallholders, deeper integration of digital, traceable supply chains, and scaling of sustainability-linked and outcome-based instruments. Ensuring that these approaches can operate at scale while maintaining financial viability and robust climate impact will be critical to closing the remaining financing gap and supporting long-term resilience in coffee-producing landscapes.

[1] National Coffee Association, History of Coffee, undated

[2] USDA, Coffee: World Markets and Trade, 2025

[3] British Coffee Association, Coffee Consumption, undated

[6] Mastai, Roasted by Climate Change: The Dire Consequences for Coffee Production, Correntics, 2023

[8] Family Farmers Climate Action, Feeding the World in a Changing Climate, 2025

[10] ODI Global, Climate change, coffee prices and production: a new macro-economic reality? 2025

[11] Ibid.